The third quarter was only 9% higher than the same period last year and the second quarter's 26% year-on-year rate of decline was much lower. Western Europe and North America's poor market Emerging markets in LCD TV shipments surpassed developed regions for the first time.

The third quarter was only 9% higher than the same period last year and the second quarter's 26% year-on-year rate of decline was much lower. Western Europe and North America's poor market Emerging markets in LCD TV shipments surpassed developed regions for the first time. In the continued quarters, it maintained a growth rate of more than 20% year-on-year. In the third quarter, global TV shipments grew only 9% year-on-year, according to the DisplaySearch Quarterly Advanced Global TV Shipment and Forecast Report. According to the latest findings, global TV shipments totaled 59.8 million units in the third quarter, which was better than expected. However, it is clear that there will be no good news for sales in North America before the end of the season, while inventory accumulated in Western Europe since the World Cup has affected shipments in the third quarter. Even in the highly developed mainland market in recent years, although the stocks in the October Golden Week have eased inventory pressure with good sales during the holiday season, the market still has some challenges in the fourth quarter.

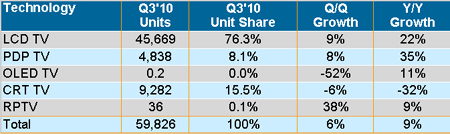

With the exception of CRT TV, all other technology TVs are growing in the third quarter. The shipment of plasma TVs grew by 35% over the same period of last year, exceeding 4.8 million units. LCD TV shipments also achieved positive growth, with shipments reaching 45.7 million units, an increase of 22% over the previous year. DLP rear-projection TVs, which are only sold in North America, were also growing in the third quarter of 2010, as consumption has paid more attention to product cost-effectiveness in the painful and slow economic recovery process. However, we believe that the fourth quarter of this year will be the quarter with the least shipment growth since the fourth quarter of 2008, as the slow recovery of the global economy has affected consumer spending on television.

“Consumers are obviously concerned about the cost-effectiveness of products, which is why plasma TVs could have such strong growth this year after a 1.5% drop in shipments in 2009,†said Hisakazu Torii, vice president of research at DisplaySeach TV. Torii further said, "The price of LCD TV panels continued to stabilize in the first half of this year, making retail prices fall more slowly, while LCD TVs with LED backlight modules also attracted some consumers' attention. For consumers, similarly sized plasma TVs have more advantages than LCD TV sales prices, making plasma TV shipments in North America during the first three quarters of 2010 increased by 39% compared to the same period of last year, compared to 40-inch and larger LCD TVs that only increased during the same period. 16%.â€

Table 1. Shipments and growth rates of global televisions by technology in the third quarter of 2010 (Unit: 1,000 units)

Source:DisplaySearch Quarterly Advanced Global TV Shipment and Forecast Report

Geographically, shipments in North America have returned to positive growth in the third quarter of 2010 after a slight decline in previous quarters, but only a 3% increase. In Western Europe, the year-on-year growth of the second quarter of 2010 was as high as 43%. However, in the third quarter of 2010, sales suddenly showed negative growth, which was a slight decrease of 1% from the same period of last year. The original optimistic expectations for the World Cup resulted in disappointing sales results. Resulting inventory correction in the third quarter of 2010. Shipments from mainland China also changed from positive growth to negative growth. The third quarter fell 2% from the same period last year. However, not all regions show a negative growth trend. Japan’s shipments have reached an annual growth rate of 62%, which is higher than the growth rate in the second quarter of 2010. This is because of the Eco-Point plan sponsored by the Japanese government. Created strong consumer demand.

Due to lower household penetration rate and gradual increase of economic conditions, emerging markets have high growth rates. In the third quarter, LCD TV shipments in emerging markets such as Eastern Europe, China, Asia Pacific, Latin America, and the Middle East and Africa exceeded for the first time North America, Japan and Western Europe have already developed markets. In the first three quarters of 2010, the growth rate of LCD TV shipments in emerging market regions was twice that of the developed markets. â€

LED backlight module LCD TV shipments slowed but continued to gain market share LCD TV shipments using LED backlight modules nearly doubled in the second quarter of 2010, but only grew 23% in the third quarter, compared to the previous quarter Increase by 5%. Using LED backlight modules LCD TVs still have a good premium space compared to CCFLs. Although the spreads continue to decline, it is still difficult for consumers to extract more money to buy high-priced TVs in the current economic environment. In some regions, such as North America, the market share of LCD TVs using LED backlight modules stopped growing in the third quarter of 2010, remaining at 21%. However, the use of LED backlight module LCD TV panel and CCFL difference is rapidly shrinking, so we can see the fourth quarter LED and CCFL LCD TV prices will be further reduced.

Samsung is the No. 1 global TV brand and maintains its leading position in LCD. Plasma TV ranks No. 2 and the top 5 rankings have not changed. Based on the revenue base, Samsung is in addition to domestic brands in the Chinese mainland market. Each area involved in the operation is the first brand. However, shipments of Samsung's LCD TVs in North America fell to second place and Vizo took the lead. In addition, Samsung’s market share fell by 3 percentage points to 21.3% in the third quarter of 2010, mainly due to the growth in the market share of brands between the 5th and 7th places.

LGE is the world’s second-ranked TV brand with a market share of 14.0%, which is a percentage point drop from the second quarter of 2010. LGE is the world’s second-largest producer of LCD TVs and plasma TVs, but has a leading position in global CRT TV revenue. The company’s revenue in this area is twice that of other brands. Sony ranked third in terms of revenue in the third quarter, down a percentage point from the previous quarter to 11.3%, but the company had better revenue growth than LGE or Samsung. Relying on its strong growth in Japan, Sharp has the strongest annual revenue growth. The company is the first brand in Japan. Panasonic is the number one brand for plasma TVs and ranks fourth among global television brands.

Table 2. Market share and growth rate of global flat TVs by revenue in the third quarter of 2010 Source: DisplaySearch Quarterly Advanced Global TV Shipment and Forecast Report

Normal Size PSU(S Series),Constant Voltage( SMV series) Co., Ltd. , http://www.chpower-supply.com