At present, the LED chip industry oligopoly has become obvious, and the industrial concentration has gradually increased. Who can dare to call the boss besides them?

In 2016, Sanan was the only one with a market share of nearly 30%.According to relevant statistics, in 2016, the scale of the entire Chinese LED chip market grew significantly, with a market size of 13.9 billion yuan, a year-on-year increase of 9%, and prices stopped falling. With the increase in the production capacity of mainland China manufacturers and the gap between technology and Taiwan, the advantages of price, delivery, and rapid market response are obvious. In 2016, the national output of LED chips increased to 76%, reaching 10.6 billion yuan. Imports were 3.3 billion yuan. In addition, with the continuous release of production capacity of mainland manufacturers, the output value of mainland chip factories in 2016 reached 11.4 billion yuan, a year-on-year increase of 13%. Due to the obvious price-performance advantage of mainland chip manufacturers, the export ratio has also increased. In 2014, the export rate was 8.9%. In 2015, the export rate was 8.1%, and in 2016 it was increased to 9.6%.

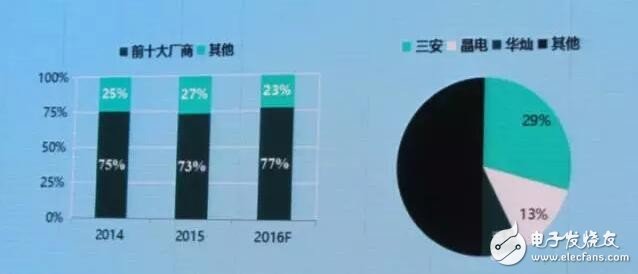

In 2016, the top ten LED chip manufacturers accounted for 77% of the overall market, with a revenue of 10.7 billion yuan, a year-on-year increase of 15%. Among them, Sanan, Jingdian, Huacan, the top three manufacturers accounted for 50% of the market, especially Sanan is in a single situation, accounting for nearly 30% of the market share.

(Image courtesy of LEDinside)

Some analysts pointed out that the mainland LED upstream chip company is basically heading towards oligopoly. By the end of 2017, the chip share of Sanan Optoelectronics + Huacan Optoelectronics will reach 70%, and the approximate ratio is Sanan 40% and Huacan 30%. There are no new entrants in the market. The old small manufacturers will soon be completely eliminated due to cost reasons. In the future, this market is played by several big factories. According to the scale, it is Sanan, Huacan and Aoyang Shunchang.

2017 price increases will also take the leadIn 2017, LED chip leader Sanan Optoelectronics first issued a price increase notice and decided to raise the price of S-30MB/S-32BB series products by 8% from January 10, 2017. Sanan Optoelectronics also publicly disclosed that the price increase was mainly affected by the backward production capacity and demand growth. After the leading price increase in the leading factory, the price of LED chips is expected to bottom out.

The price has risen. On the one hand, the contraction of the supply end of the LED industry is a very important driving factor for price increase. In fact, the improvement of the supply pattern has a very large impact on prices. For example, last year's supply-side reforms have greatly increased the prices of industrial products. On the other hand, the price increase of upstream materials is more obvious. This year, the PPI is at a high level. Since many of the materials required for LEDs belong to industrial metals, the price of industrial metals is rising from the previous month, and it can be inferred that prices will continue to rise.

From the big trend, the 2017 chip continues to rise is a foregone conclusion. Industry experts expect that the price increase of LED chips will continue until the third quarter, and will decline slightly in the fourth quarter. The annual increase will reach double digits, so the price increase of the lamp will continue until the third quarter of 2017. The rise in the price of LED chips is driving the mid-stream and downstream industries to “price surgesâ€.

Who must have in the 2017 arms race?Huacan Optoelectronics

Recently, it has announced that it will invest 6 billion yuan in Huacan Optoelectronics. It is expected that the new plant in Yiwu will be put into production in May 2017, and will reach an annual output of 3 million LED chips.

Sanan Optoelectronics

With the expansion of Huacan's expansion, it is said that Sanan will not be outdone. In order to maintain its leading position, it will also purchase a large number of machines in 2017. In addition to blue LEDs, the expansion project will also target high profits. The quaternary LED capacity is expanded.

Aoyang Shunchang

Aoyang Shunchang has accelerated the expansion of LED die production in the second half of 2016. It is expected to gradually release production capacity from the first quarter of 2017. The production capacity in 2017 is expected to reach 800,000 pieces per month.

Dry photo photoelectric

In addition, the dry photo optoelectronics started with the four-element LED is reported to have increased the production capacity of the four-element LED machine in 2017.

Equipment manufacturers also revealed that the current domestic LED chip factory expansion is to introduce a new 4-inch machine, 4 inch Lei wafer is equivalent to 4 times 2 inches, if each month's production capacity is about 4 inches 3800 ~ 4000 pieces of epitaxy Look, it is expected that by 2017, LED die production capacity will enter a new round of explosion. Together with OSRAM's Malaysian plant is about to be completed, huge capacity will be released in 2017.

China LED chip factory main capacity list

According to Guoxin Securities analysis, in 2017, LED chip leading enterprises increased by about 345 units (converted VeecoK465i model 54-piece machine). Including the improvement of the old models that purchased some used equipment, the global effective capacity at the end of 2017 reached 83.28 million pieces/year. In 2017, the demand for chips was 92.35 million pieces, an increase of 12.5%. Among them, the demand for lighting chips increased by 20% to 47.04 million pieces; the demand for outdoor full-color display screens increased by 5%; the demand for small indoor distances increased by 50%; the demand for mobile phone backlights was 1.39 million; the demand for backlights for tablet computers was 440,000. Film; computer and TV backlighting demand 6.99 million; automotive lighting demand 1.06 million; other about 8.39 million.

Guosen Securities believes that any industry production capacity is slightly higher than demand is the steady state characteristics of supply and demand balance, and LED demand is still stable at 12.5% ​​in 2017, so Guosen Securities judged: 2017 LED chips are in short supply, LED chips at the end of 2017 The effective capacity is about 83.28 million pieces and the demand is about 92.35 million pieces.

Who are they? Sanan

Sanan Optoelectronics LED chip industry is in the domestic leading position, with all visible and invisible LED chip products, the company's technical capabilities and product quality in China, has been in Taiwan's crystal power shoulders, and gradually narrow the gap with European and American products. The company's domestic market share is about 30%. It is expected that the company will expand production by 33% in 2017 and reach 2 million pieces/month by the end of the year. It is expected that the scale of revenue will surpass that of Jingdian and become the international leader of LED chips.

The company continues to acquire self-supply capabilities of sapphire, hydrogen, nitrogen and other chip raw materials in the upstream through investment, acquisition, joint venture, etc.; downstream establishes joint ventures such as LED lighting and automotive applications to open downstream sales links. Through the upstream and downstream core industry chain layout, vertical integration brings excellent cost control and downstream bargaining power. The gross profit margin is expected to reach 40% in 2016, far higher than the industry average.

In 2015, the company announced the construction of a 300,000/year 6-inch GaAs production line and a 60,000/year 6-inch GaN production line to lay out compound semiconductors. GaAs and GaN are the stars of the second and third generation semiconductor materials respectively. At present, the company has obtained military customer procurement agreements and bulk shipments of domestic large customers. At the end of 2016, we will obtain technical licenses through cooperation with GCS, and will further expand domestic and foreign customers in 2017.

With the rise of 5G, IoT, electric vehicles, smart cars and other application markets, the global market for gallium arsenide/GaN devices is expected to exceed 70 billion yuan in 2021. At the same time, China's chips rely heavily on imports. Taking China's smart phones as an example, more than 90% of gallium arsenide/gallium nitride chips need to be imported. Sanan Optoelectronics production line will fill the domestic gallium arsenide/gallium nitride blank and is expected to replace imported chips. Independently control China's "core". The company has benefited significantly from the support of the national industrial policy, and has obtained state financial support and a collection of outstanding talents at home and abroad.

Huacan

Compared with the leading Sanan Optoelectronics, Huacan Optoelectronics has a smaller market value and better elasticity. At present, the market value of Sanan Optoelectronics is 66 billion. As the second in the industry of LED chips, the market value of Huacan Optoelectronics is expected to further increase in the future. At present, the monthly production capacity is 700,000 pieces, and there is a Yiwu base with a capacity of 1 million pieces per month. It will be gradually put into production in July this year. In the field of display applications, Huacan Optoelectronics' LED chips account for more than one-third of the domestic market.

In 2016, Huacan Optoelectronics' revenue grew rapidly. On the one hand, due to the completion of the merger and acquisition of upstream sapphire substrate supplier Lanjing Technology in May 2016, Blue Crystal consolidated its revenue by 231 million yuan, deducting the influence of Blue Crystal. In 2016, the company achieved revenue of 1.351 billion yuan, a year-on-year increase of 41.5%. On the other hand, due to the completion of the company's LED upgrade project, the scale of production and sales increased significantly, and the sales volume of LED chip products increased by 130.96%.

The profitability of Huacan Optoelectronics LED business has improved significantly. The gross profit margin of products in 2016 was 24.05%, which was 7.3 percentage points higher than last year. The gross profit margin of Q4 products was 29.77%. In 2016, the LED chip industry shuffled, the backward production capacity was eliminated, and the price competition returned to rationality. Huacan Optoelectronics LED chip products benefited from the rapid growth of the market demand for small-pitch display screens, and the price increased steadily; The company's profitability has improved. The gross profit margin of the company's 16H2 blue LED was 25.4%, up 12.6 percentage points over 16H1; the gross profit margin of green LED chips was 24.2%, up 19.4 percentage points from 16H1.

In addition, Huacan Optoelectronics plans to acquire a new journey in the field of sensor innovation. The company plans to issue 237 million shares and indirectly complete the acquisition of the world's leading MEMS company, Meixin Semiconductor, at a price of 1.65 billion yuan, thus entering the field of MEMS sensors. The new products are concentrated in the field of inertial sensors, and their products are widely used in the automotive and consumer electronics fields.

Portable Megaphone,High Quality Megaphone,Wifi Megaphone,Megaphone Small

yucheng county huibang electric technology ltd , https://www.hbspeaker.com